A space to learn more about personal financial planning. You can expect regular posts covering a range of topics from tips & tricks, to big decisions that matter for DB Pension Members, Incorporated Business Owners, DIY Investors, and those making big life pivots.

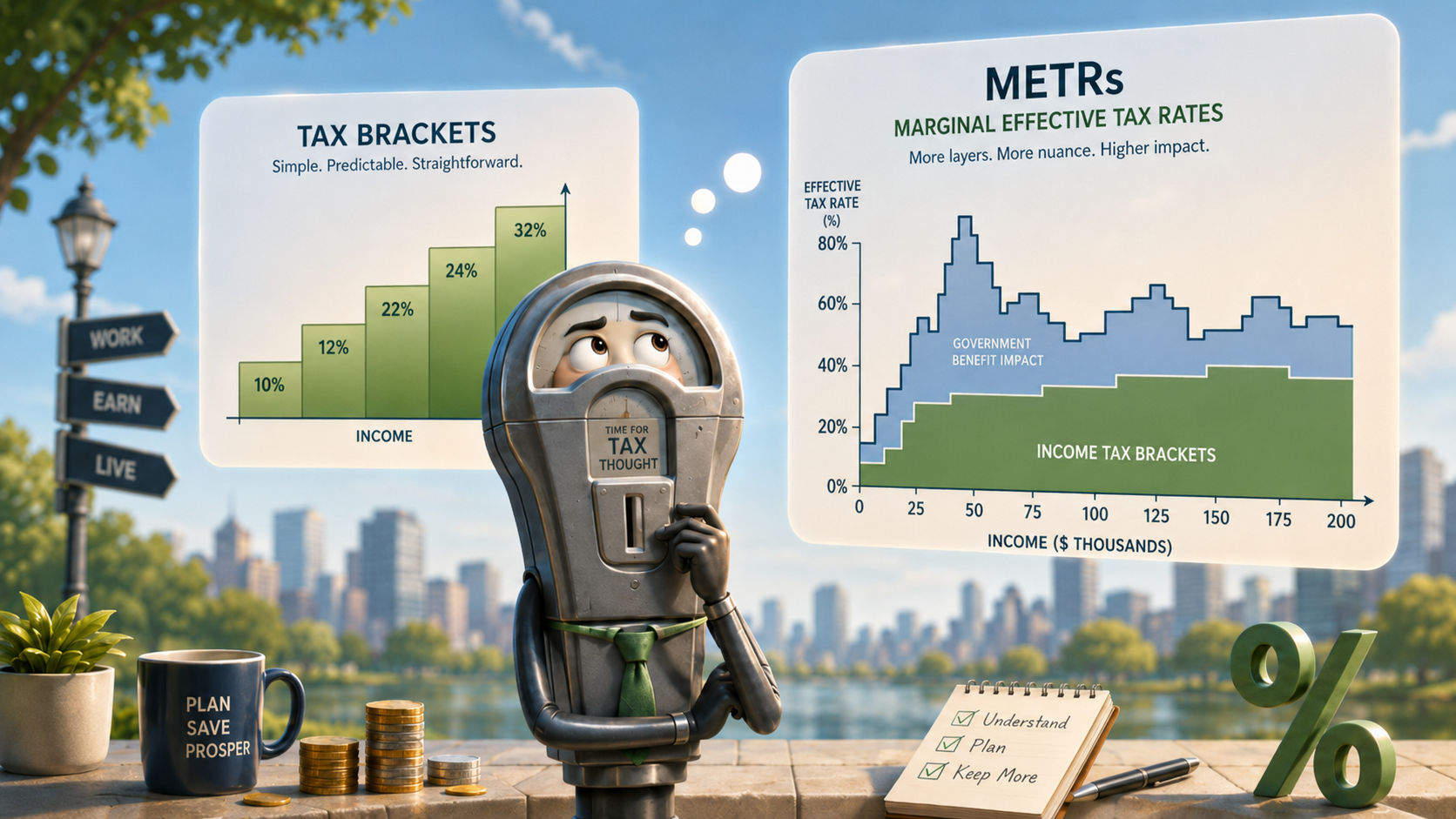

What’s your M.E.T.R.? … and other ways “managing income to a tax bracket” can go wrong.

Planning taxable income around a certain tax bracket often misses nuances in how income is calculated, tax deductions, and finally income tested government benefits. It’s an effective and valuable process but not as simple as just eyeballing a tax bracket and hoping you end up close to that.

This post summarizes some of the pitfalls I have seen for clients trying this approach on their own.

“I try to keep my taxable income under the “X”K combined tax bracket” sounds smart and can make great sense if done correctly, and for the right set of circumstances

Managing your taxable income to a bracket sounds simple but almost everyone I’ve worked so far who is attempting to manage taxable income (even with the help of accountants) is missing some part of the required nuance. It’s tricky stuff, and requires a deep and reasonably comprehensive multi-year understanding of your finances and life.

But first one big caveat, this article is not personalized tax advice, many details and nuances are omitted for simplicity. It’s a framework for how to think about annual taxable income planning from someone who came from outside the personal finance world and has had to learn it (I’m still learning every day).

First in order to manage your income you need some control over it. The degree of control you have over your taxable income varies a lot depending on your personal situation including:

How much cash flow do you need to live on (If you need to spend everything you earn and don’t have other resources taxable income planning will be difficult)?

Are you adding to, repositioning, or withdrawing from your investments?

Does your income naturally vary from year to year and can you earn more/less on demand?

What type(s) of income do you have (investments, employment, business etc.)?

What tax deductions (if any) are available to you

Generally the more of the above are true the more opportunity you will have for taxable income planning. But most Canadians have some opportunity to manage their income through RRSP contributions and eventual withdrawals.

Why might you manage your taxable income if you could?

Canada has a progressive taxable income system, in general lower taxable income that is smoothed across years and more evenly split amongst partners delivers a more efficient result than very high or lumpy income. Consider 2 example families that both earn 400K in total household income over 2 years (all employment income in Ontario and ignoring gov’t benefits for simplicity). Family 1 has one partner earn 400K in year 1 and both partners earn zero in year 2 , family 2 has 2 partners working for 2 years each for 100K/year. Family 2 will pay nearly ~70K less in personal income taxes, leaving more money to live and invest.

I find most clients intuitively understand this part, it’s what gives rise to the desire to do some taxable income planning e.g. avoiding the nearly 54% marginal tax rate on taxable income above ~258K, or the ~5.5% income tax rate jump on income above ~117K. For those who do have significant ability to manage their taxable income there are strong benefits to doing so. The problem is that there are a couple of wrinkles that many DIY tax planning efforts miss notably: Tax treatments of different types of incomes, tax deductions, and income-tested government benefits.

This is a nuanced topic (And I will necessarily leave out a bunch of details) but I’ll do my best to highlight the most common misinterpretations when estimating your tax bracket for income planning purposes. There’s a whole separate set of considerations for what deductions you may be entitled to, and how you might try and legally split income with a partner or stage it over multiple years (also important but not for today!).

Wrinkle 1: Estimating taxable income.

The first complication is that not all types of income are treated the same when calculating taxable income. Employment income and interest income are generally included dollar-for-dollar.

Eligible dividends from taxable Canadian corporations — for example, dividends from public companies such as TD Bank or Enbridge — are treated differently. These dividends are “grossed up” by 38%, meaning that $1.00 of eligible dividends counts as $1.38 of taxable income. This does not mean eligible dividends are necessarily taxed more heavily overall. The gross-up is paired with a dividend tax credit, which is intended to recognize that corporate tax has already been paid. However, that credit reduces tax payable after taxable income has already been calculated. This distinction matters when taxable income itself affects other calculations, thresholds, credits, or benefits.

Realized capital gains (think from the sale of taxable investments or a second property) have 50% of the gain included in taxable income.

So for a hypothetical couple who work together in a family business and where each family member has a 70K salary, 20K of eligible dividends received, 10K ineligible dividends, and a 50K capital gain on the sale of their portion of a jointly owned rental property there’s some nuance to their income estimation. For those following the math it would be 70K + 1.38*20K + 1.15×10K + 50%*50K = 134.1K of income for tax purposes before considering deductions.

There’s then a second step of calculating deductions which serve to reduce taxable income. Two frequent deductions are RRSP contributions, and eligible childcare expenses but there are many more. Deductions reduce your taxable income dollar for dollar (subject to the cap on the deduction). Let’s imagine one of our family members was planning to deduct 10K in RRSP contributions and is eligible to deduct 10K in daycare expenses (only available to the lower earner). Now their taxable income is $114K. They might compare that to the combined tax brackets in Ontario and say, great I’m just under the ~117K cutoff for the next tax bracket (and from jumping to an over 43% marginal tax). And my RRSP deduction is primarily coming from the above 117K tax bracket thus reducing my current tax bill by 43% for every dollar contributed. But even if they managed to do all of the above correct they might still be missing some nuance: Enter income tested government Benefits

Before we go there though between the 2 steps above, someone who is “ballpark estimating” their taxable income can go significantly awry so doing a mid-year check with an accountant or financial planner before making any big moves like triggering capital gains or paying yourself a bonus can definitely help!

Now for Wrinkle 2: Income tested government benefits

The Federal and Provincial Governments offers many generous benefits for taxpayers. Many of these benefits are “Income-tested” meaning that they stop or are gradually “clawed-back” as your personal net taxable income or adjusted family net income (AFNI) exceed certain thresholds. The tricky part is that the cutoffs for these benefits don’t always match up with the tax brackets you may have been planning for, and the way they are calculated varies by benefit as does the benefit year.

A DIY tax planner might compare their 114K personal taxable income that to the combined federal/Ontario tax brackets and say, “Great, I’m just under the roughly $117K threshold where the marginal rate on ordinary income jumps from about 38% to about 43%.” That may be a useful observation, but it still may not tell the whole story. The tax bracket is only one layer. The next layer is whether the same income affects income-tested government benefits, credits, or clawbacks.

The most famous example is the infamous OAS Recovery Tax. For July 2026-June 2027 payments the government will “Claw back” 15% of your OAS payments for every dollar of 2025 personal worldwide net income that exceeds the cutoff of $93,454. So for your next dollar earned above this threshold in addition to personal income tax of ~43% you’d be losing 15% of your OAS benefit. This means your marginal effective tax rate (M.E.T.R) inclusive of government benefits could be ~58% which is even higher than the top combined federal/provincial personal tax bracket. My personal view is that it is good policy not to pay OAS to seniors who don’t need it, but the current system sure does create some strange incentives and tax complications.

Now our dual earning couple above was a long way from retirement, but they do have 3 children under age 6 and are eligible for the Canada Child Benefit which is an income tested benefit based on Adjusted Family Net Income. I’ll save the details for another post but even at ~228K of AFNI they are still entitled to ~$4K/year in tax free Canada Child Benefit Payments. And more interesting is that their Marginal effective tax rate is 8% higher than a simple “tax bracket analysis” would suggest.

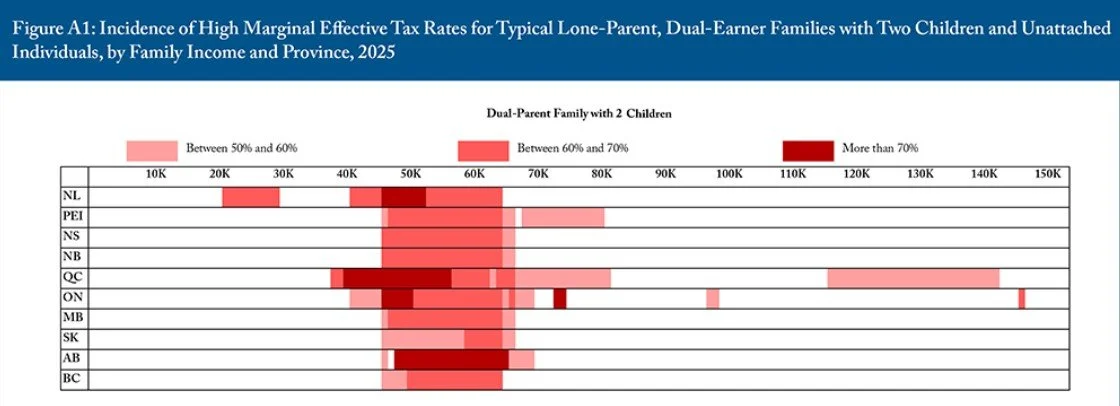

Canadians who are most likely to see the the biggest differences in their marginal effective tax-rates and their simple tax brackets are parents with modest incomes, and single income seniors who are close to the OAS Clawback Thresholds.

I find this visual extremely helpful from the CD Howe Report “The Clawback Trap” which shows how M.E.T.R.s can exceed 50% for 2 child modest income households (Whom traditional financial advice would say never contribute to your RRSP when you are in a low tax bracket). Link to the report here: https://cdhowe.org/publication/the-clawback-trap-how-canadas-benefit-system-can-undermine-work-and-saving/

There are many other benefits, especially if you will have a modest family or personal income (see above the 40K-80K) AFNI range is pretty severely taxed on a M.E.T.R. basis across Canada for parents.

Finally, life changes, and financial and tax-planning should be a long-term focused process that anticipates a certain amount of uncertainty. It doesn’t do much good to perfectly fit into a desired tax bracket for 3 years only to blow past it by orders of magnitude to cover a major expense in the 4th year. This is where wholistic multi-year planning can make a big difference.

All this is to say that DIY tax planning is helpful, but it’s rarely as simple as “I just pay myself $xK to stay below the $yK tax bracket”.

If you found this article helpful please subscribe and/or share it with your friends and family and broader network, it really helps me continue to write these.

Finally if you think annual taxable income planning might be appropriate for your situation, but I’ve successfully talked you out of doing it without some help, I am currently including annual taxable income consultations for all of my ongoing advice-only financial planning clients you can book a complimentary introductory video call here.

When Is Ongoing Advice-Only Financial Planning Worth It?

I do not think everyone needs ongoing financial planning. The hypothetical couple in my last case study likely could have done well with a focused planning engagement and then revisiting things periodically as life changed. Ongoing advice has real benefits — financial and emotional — but those benefits need to justify the ongoing cost.

So who benefits most from ongoing planning? I think the case gets stronger when one or more of the following conditions are present:

There is complexity and choice

You are in or approaching a major transition

The stakes are high

There is significant follow-through or behavioural change required

In my last blog post I looked at the cost of ongoing advice-only financial planning compared to more traditional assets-under-management advice models. I used that comparison because they are more comparable in terms of fees and service: both are meant to provide ongoing proactive support, just paid for differently.

Let’s first define Ongoing Advice-only planning as an annual retainer agreement where the planner supports the client in identifying, measuring, and executing on their financial goals but does not sell any products, manage investments, or take a percentage of those investments. Instead the client pays directly for an annual retainer. The alternative (and popular) model is a project-based fee, for a fixed timeline and set of deliverables or hourly support.

From a planner’s perspective, a recurring relationship is obviously attractive. It creates continuity, makes deeper planning possible, and avoids constantly needing to find new clients. But from a client’s perspective, the more important question is whether ongoing advice is actually the best value.

Over the past several months my perspective on this has sharpened. I do not think everyone needs ongoing financial planning. The hypothetical couple in my last case study likely could have done well with a focused planning engagement and then revisiting things periodically as life changed. Ongoing advice has real benefits — financial and emotional — but those benefits need to justify the ongoing cost.

So who benefits most from ongoing planning? I think the case gets stronger when one or more of the following conditions are present:

There is complexity and choice

You are in or approaching a major transition

The stakes are high

There is significant follow-through or behavioural change required

1. There is complexity and choice

If your income, expenses, and savings are relatively stable and your key risks are protected (insurance, wills etc.) then for a period of time aligning on a targeted savings rate, sticking to it, and investing in low-cost globally diversified funds might be all you need (kind of like a doctor’s or mechanic’s visit, save X$ per year into account Y and check back in 3-5 years or if something big changes).

Others have “complexity factors” that allow for greater degrees of freedom in where they choose to save, spend, invest etc. some of these include:

Flexibility in determining your income and sources of income (e.g. business owners, pension deferrals, retirees withdrawing from RRSPs/RRIFs, realizing gains on investments, deciding if/when to claim certain government benefits)

Weighing paying down significant debt against non-registered investments or savings

Variable income either through business ownership, sales commissions, bonuses, stock-based compensation, trust distributions, or inheritances

Education savings for children or large infrequent purchases

Disabilities, or leaves of absence from work in the family etc.

Defined benefit pensions and the option to purchase leaves of absence(s), take a new role etc.

The “right advice” for handling these situations is very personal and can evolve over time, even for the same person. Once there’s enough complexity at play, an integrated and consistently updated financial plan becomes increasingly valuable both financially and psychologically. Each time a planner “picks up your file,” there’s a fixed cost in time and money to get re-familiarized. If you have enough complexity and enough decisions, it may be more cost effective to have someone who knows your situation cold and is working proactively to help you meet your goals faster.

2. You are in or approaching a major transition

Planning is often the most impactful on both ends of major life transitions

Some common examples include a career change, starting or selling a business, buying or selling a home, receiving an inheritance, giving money to children, approaching retirement, losing a spouse, or deciding to work less.

These moments often create clusters of important decisions, and those decisions are not always purely financial. They can be emotional, personal, and time-sensitive. It’s also in these periods of transition that we often gain more clarity about our goals and what really matters (which should be reflected in your financial plan).

Retirement is probably the most common example. The question is rarely just “can I retire?” It is usually some version of: “what would make me comfortable enough to actually start spending the money I saved?” The math matters, but so does the personal side. How much flexibility do you want? What would make retirement feel successful? How would you feel if you had to change your spending during retirement or downsize your home? How much do you want to preserve for the next generation?

This is why “approaching” a transition matters. Waiting until after the transition has happened can mean some decisions are already constrained.

3. The stakes are high

This one is somewhat intuitive, but it is also a feature of a largely fixed-fee business model. If a family with a net worth of $3 million, or a household income of $300K+, is paying a ~$4K annual advice-only planning fee, it is often easier to find tax, investment, or behavioural opportunities that more than cover the cost of the fee. While I have seen a few high-value, low-income planning opportunities (often centered around government benefits) they are usually best served by project based work.

High-stakes decisions often overlap with transitions and complexity, but not always. A household with a large taxable portfolio, the opportunity to buy back pensionable service, significant corporate assets, or meaningful annual surplus may have ongoing planning opportunities even if life is otherwise fairly stable.

4. There is significant follow-through, behavioural change, or education required

This may be the most underestimated source of value in ongoing planning. Many people roughly know what they should be doing: save more, spend more intentionally, simplify investments, reduce unnecessary taxes, update estate documents, review insurance, or make the decision they have been putting off. But the issue is not always knowledge. Sometimes it is confidence, behaviour, or follow-through.

One area I have seen this clearly is with very good savers approaching or entering retirement. On paper, the math may show that they can afford to spend more, retire earlier, help children, travel, or make a meaningful gift. But after decades of saving and being careful, actually using the money can feel uncomfortable.In those cases, the planning work is not just about proving that the money is there. It is about helping clients build enough confidence in the plan to change behaviour.

Education can create a bit of a flywheel here. As clients better understand their situation, they often become more confident. As they become more confident, they can become more ambitious and creative with their goals. Instead of simply asking “are we okay?” the conversation can shift toward “what do we actually want this money to do”? That can lead to much better use of money. Not necessarily more spending for its own sake, but more intentional spending, giving, lifestyle design, or risk-taking where it actually aligns with the client’s goals.

There is also the practical implementation side. A good plan can still fail if the actions do not happen. Beneficiary designations need to be updated. Estate documents need to be reviewed. Investment accounts need to be simplified. Cash flow systems need to be set up. Corporate and personal planning may need to be coordinated with an accountant. None of this is especially glamorous, but it matters.

For some clients, the value of ongoing planning is not that we uncover a brilliant new strategy every year. It is that there is a structure in place to keep moving the important things forward, while continuing to refine the plan as their understanding and goals evolve.

In summary ongoing Advice-only planning is most valuable when the plan (or your life) is unlikely to stay static

If your situation is evolving, the decisions are meaningful, or the real work is turning good intentions into action, then ongoing planning can be worth exploring. If not, a focused engagement and revisiting things as life changes may be the better fit.

At Gybe, the goal is not to make every client an ongoing client. The goal is to match the planning relationship to the situation. If you would like help figuring out what level of support makes sense for you, you can book a complimentary introductory video call here.

If you found this article helpful please subscribe and/or share it with your friends and family.

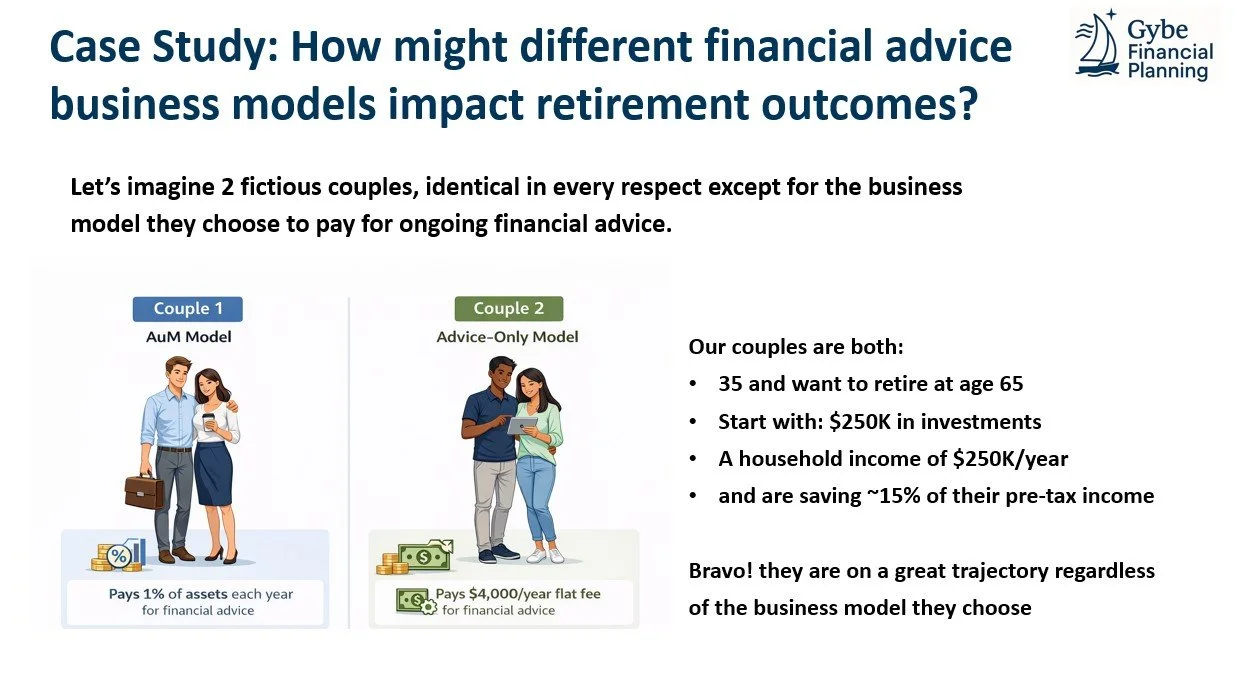

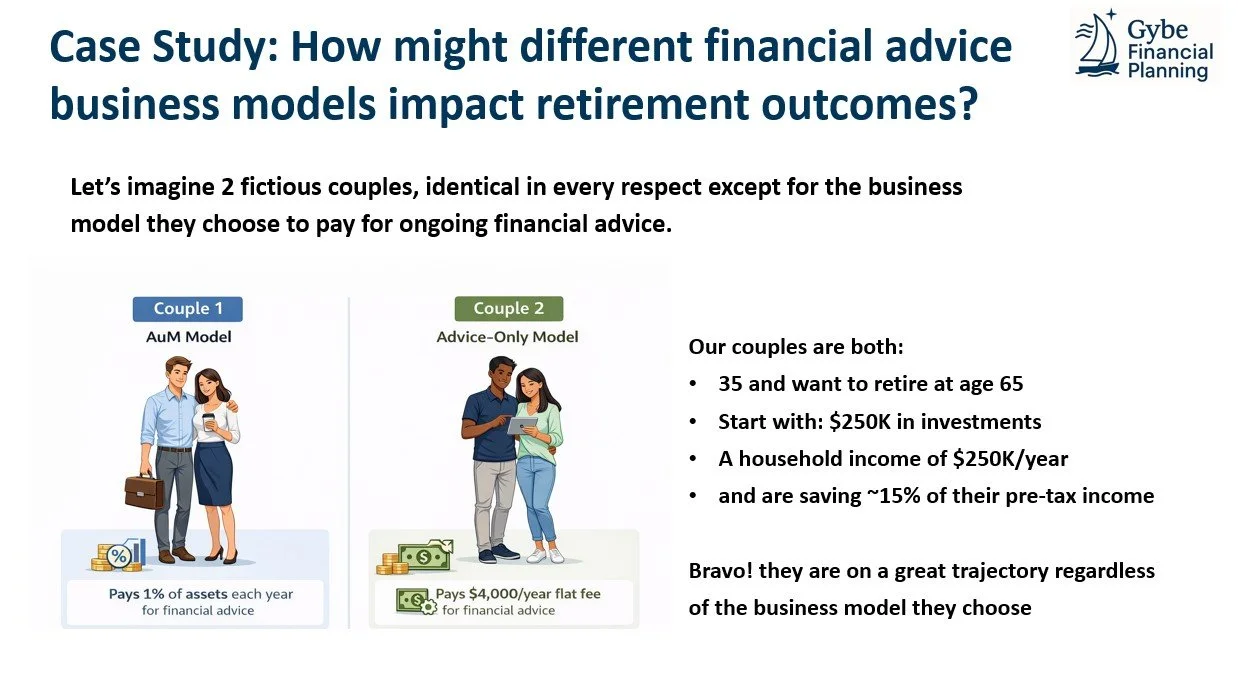

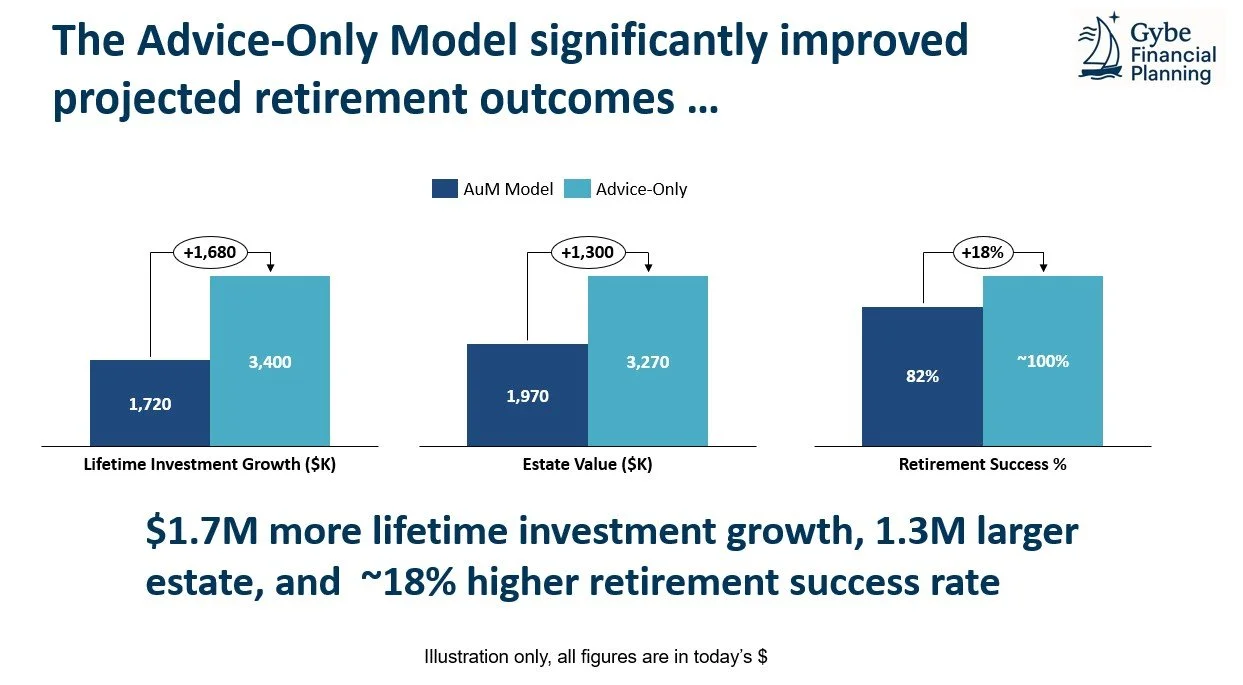

Could Ongoing Advice Only Planning help improve your retirement outcomes? A case study on the cost of advice.

How you pay for financial advice could impact your retirement. A fixed fee, advice-only retainer added $1.7M in lifetime investment growth for the couple in this case study. Plus see blog for bonus content on different advice models.

We’ve covered in previous blog posts that high investment costs and straying from evidence-based investing are typically a losing proposition for investors.

I want to be careful to clearly delineate the cost and potential value of financial planning and advice (and not simply paying for investment management).

A good planner can help you tease out your financial goals, build wealth efficiently, save on taxes , and put major life decisions in the context of your financial life. The peace of mind and accountability partnership can be the difference in achieving your financial goals and for many people is well worth paying for. There’s a mix of hard $ savings and returns and soft benefits and it’s impossible to quantify in advance, but my experience so far has been a very high return on investment relative to initial planning fees.

Ok so if paying for high quality ongoing personalized financial advice can make sense for some people, what does it actually cost and how do those costs impact your financial outcomes?

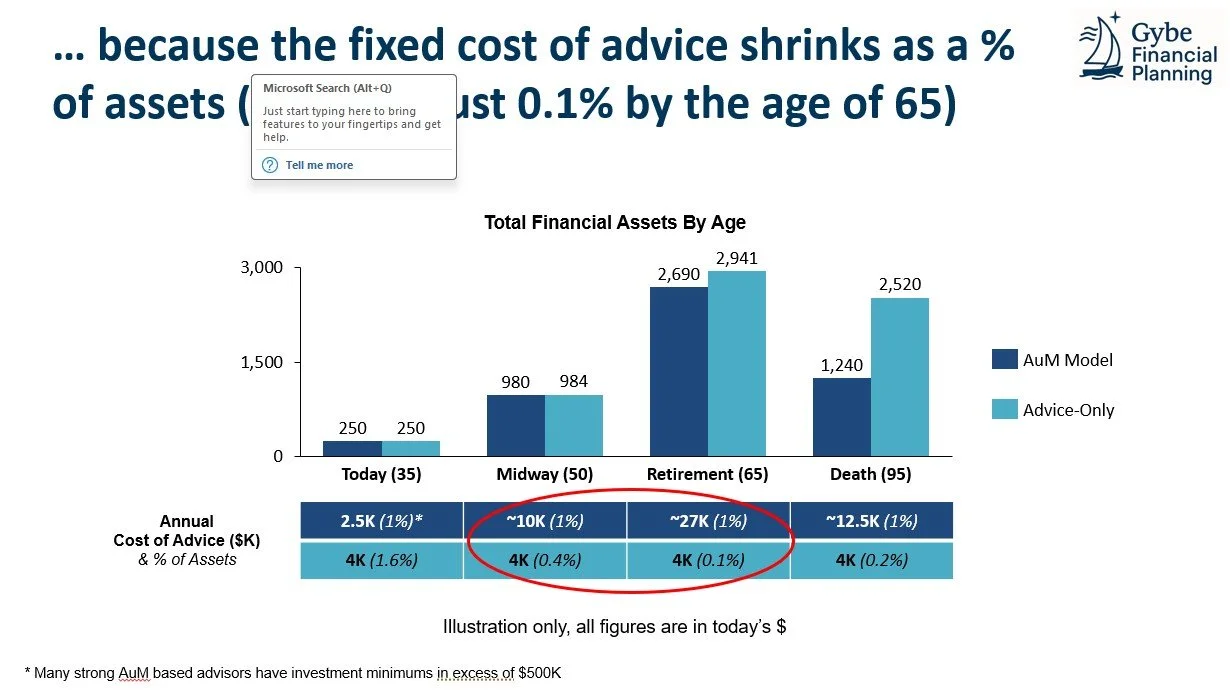

It made sense intuitively that once you have a higher value of assets paying a fixed fee versus a % of assets would likely be more cost effective, but It wasn’t immediately obvious to me that paying a fixed fee over your lifetime would potentially lead to better retirement outcomes. So I decided to test it with a good old fashioned case study.

An Important simplifying assumption I am making is that their before fee-performance is identical as are the financial moves they make in their life (based in part on the quality of the advice) are equal. I think this is totally possible for disciplined self-directed investors but many are not able to avoid tinkering.

These are definitely not identical services, nor are they the only ways Canadians can arrange their personal finances, but it’s helpful to know on cost-only basis how these different service models compare.

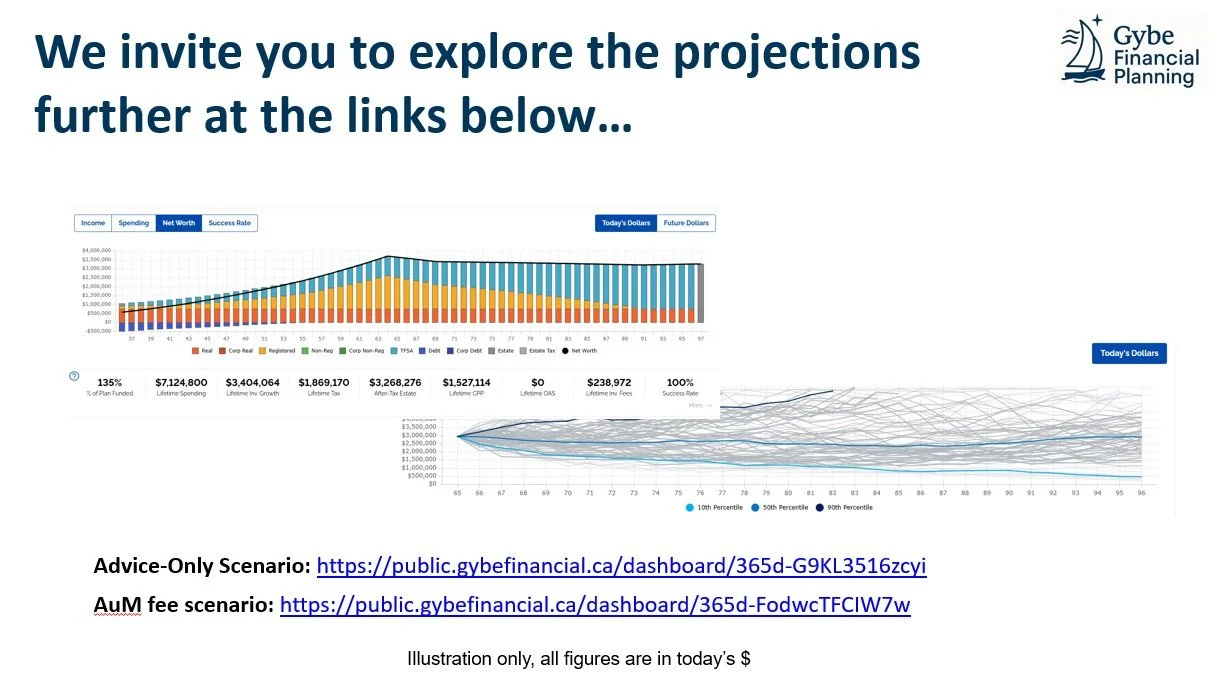

For those interested in the more detailed assumptions and/or exploring the modelling software you can download the case study slides here

As a bonus below I’ve outlined several “options” that exist for Canadians in accessing advice and their typical costs

Option 1-Investment Manager that focuses on high cost (proprietary products) or active investing (picking stocks)my personal view is that even high quality comprehensive planning would struggle to overcome ~2%+ ongoing fees from a financial outcome standpoint: Please refer to my previous blog post… and don’t do this!

Option 2-Investment Manager that focuses on low-cost evidence based investing and comprehensive financial planning. Typical cost is ~1% of assets under management for advice and another ~0.2% for investment implementation. This way you are mostly paying for advice, which can be very valuable. This is a great option for many, especially if you aren’t comfortable managing your own investments and/or would be tempted to sell in market downturns. One such example is PWL Capital whose Chief Investment Officer Ben Felix, is one of the premiere personal finance educators. There are significant synergies in combining financial planning and investment management including dynamic withdrawal strategies.

Option 3- Ongoing Advice-Only Financial Planning (AoP). This is often a “fixed fee” model of ~2,500-5,000+ per year which on significant investment balances can be much less than 1% per year. The level of planning (and hence value add) is also usually directly related to the fees charged. In this model the client manages their own investments or pays separately for investment management. Most AoP planners are not securities licensed and cannot discuss or recommend specific investments but can add value on asset allocation and assessing the costs of your current investments.

Option 4- Do it Yourself Investments and/or Robo-Advisors (No/Limited Advice): I’ll be the first to admit, not everyone needs to pay for advice. Self-directed investing can be had for 0.1%-0.5% of your assets. For many people especially those in their early accumulation phase, who are already on a strong track of saving in their registered accounts, and have the temperament to stick to a low-cost buy and hold investment strategy this can be a great option. It’s where things start to get complicated (either through registered accounts maxing out, contemplating big changes in income, self employment or incorporation, managing an inheritance, or thinking about retirement dates and retirement income planning) where thoughtful advice can really shine.

If an ongoing advice-only financial planning model could make sense for you, you’ve come to the right place

At Gybe most clients we have partnered with so far have had short-term financial opportunities that are significantly larger than the initial financial planning fee. Relatively simple strategies have brought our clients years closer to achieving their financial goals, which has been great validation for the business model. It’s also why to date Gybe has been offering clients a 100% unconditional money-back guarantee on our financial planning services (and we haven’t had any issues yet). If you’d like to explore what a 90-day financial planning engagement might look like for your situation please book a complimentary introductory session here

If you found this article helpful please subscribe and/or share it with your friends and family.

Does your investment portfolio have these five hallmarks of being evidence-based?

Does your investment portfolio have these five hallmarks of being evidence-based?

Reflections on the five hallmarks of an evidence based investment portfolio.

1) Simple, 2) Passively Managed, 3) Low Cost, 4) Globally Diversified 5) Appropriate Asset Allocation

Photo by Towfiqu barbhuiya on Unsplash

I spent the first 10+ years of my career as a consultant to the investment teams of several of Canada’s largest pension plans. These organizations have access to incredible talent, scale, and cutting edge research. They hire teams of the best and brightest, and work hard to deliver a globally diversified portfolio with slightly enhanced risk-adjusted returns — net of the costs of all those smart people & technology. While there have been some recent challenges, it’s still a model that intuitively makes sense: world class investment managers, with massive scale, working on behalf of their members, without a profit motive.

Unfortunately, most individuals don’t have the option to invest their full savings alongside the $200 Billion+ behemoths like PSP, OTPP, or CPP Investments.

Over the past few years I’ve delved into the research on what investment approaches work best for individual investors and the good news is that excellent returns don’t require pension level knowledge, scale, expertise, or complexity.

The more I learn, the more I am convinced that for long-term individual investors a simple, passively managed, low-cost, globally diversified, portfolio with an appropriate asset allocation is ideal in the vast majority of cases.

As a reminder this blog is intended as general education and is not investment advice.

I’ve summarized what I’ve learned into five hallmarks of an evidence-based investment approach:

1) Simple—> As few moving parts as possible. The more moving pieces and complexity the more trades and decisions that need to be made both in rebalancing and investing new contributions. It’s extremely difficult to beat the market, so each time an investor tinkers with their portfolio they’re likely to lose a little (or a lot). Fewer moving pieces (all else equal) leads to performance that stays closer to the market, and market performance is pretty remarkable! This might literally mean holding a single exchange traded fund or low-cost mutual fund in your portfolio.

2) Passively Managed—> Not trying to beat or time the market. This applies at two levels. #1) In the funds that you invest in: There is evidence of skill amongst the most skilled investment managers; however it’s nearly impossible to identify that skill in advance, and the fees those managers charge (to retail investors) tend to eliminate any outperformance, so you are better off not paying someone to try and beat it and instead owning the market through an broad index fund. #2) In how you engage with your investment portfolio, even passively managed funds can be used to time the market in an active way (think selling your holdings when there are scary news headlines). Again each change you make is a gamble against the really smart people who make up the market. There is some evidence supporting factor based investment approaches (e.g. Value & Size) but these should be systematically applied to a portfolio that still has broad market exposure.

3) Low-Cost—> Less than 0.5% for investment management implementation. As discussed in a previous post, costs can significantly impact your long-run investment outcomes. For many people paying for advice including financial planning can be very valuable (quantitatively and qualitatively), but that should be considered separately from the cost of pure investment implementation which should be less than 0.5% (and often ~0.2%).

4)Globally Diversified—> Holding the whole global market. Diversification is the only “free lunch” in investing: higher expected returns without increasing the level of risk. Broad diversification across many geographies and size of companies and individual holdings helps smooth out the ride. By casting a broad net you are more likely to catch the winners (and the losers but that’s ok) and the winners tend to drive overall market performance.

5) Appropriate Asset Allocation—> A personalized mix of stocks & bonds. This is probably the most important decision an investor must make — and continue to evaluate over time— essentially what % of your investments do you hold in each of equities and fixed income. All else equal more stocks means higher expected returns, but also higher volatility. There’s no universal right answer, but having an asset allocation that fits your plan and that you can stick to in poor markets is critical.

Individual investors they can achieve all five of these hallmarks by holding a single asset-allocation exchange traded fund (ETF) across all of their registered and non-registered accounts.

I won’t list the names of individual securities here but two of the largest providers are Vanguard and Blackrock and they offer “Conservative”, “Balanced”, “Growth”, and “All Equity” exchange traded funds that can give you all of the hallmarks above for <0.25% for self-directed investors. There’s a helpful comparison of the funds here: https://www.looniedoctor.ca/best-asset-allocation-etf/. If you aren’t comfortable making your own trades most robo-advisors implement a similar approach and cost ~0.5%.

There’s even a rapidly growing trend of investment advisors and financial planners putting their clients in asset allocation funds so they can focus more on financial planning instead of trying to beat the market.

For some very experienced individual investors with large portfolios ($500K+) asset location strategies (considering the after-tax impact of holding different securities in different accounts) and/or directly holding the underlying funds of an asset allocation fund might yield better after-tax performance. The big might here is that behavioral biases and/or rebalancing issues could easily offset the gains to be had, and there’s a significant time commitment involved.

PS the Rational Reminder podcast has been my go-to source for diving deep on evidence based investing: https://rationalreminder.ca/, they frequently host leading academics and world class investors. If you are just getting started learning about investments this episode is a great place to start: https://rationalreminder.ca/podcast/381

Have questions or want to talk about what this means for your personal situation? Book a free consultation or send me a note at chaz@gybefinancial.ca.

If you found this article helpful please subscribe and/or share it with your friends and family who could benefit (I send a maximum of one article per month).

What are Canadians actually paying for investment management and financial advice? And what are they getting?

Thanks to growing awareness and marketing Canadians are increasingly skeptical of high investment fees. But what really goes into investment management fees? What is the average Canadian Investor paying and what are they getting?

Fees matter and Canadians are starting to notice: Let’s start with a classic Questrade commercial outlining the impact of fees on investment returns: Compound Interest the 8th wonder of the world. The commercial is emotionally powerful, and compares an investor paying 2% fees over 30 years and ending up with ~400K (or ~40%) less at retirement.

But do Canadians really pay 2% fees? And if so what are they getting for those fees? This is a more complex topic than meets the eye, and I’ll start to chip away at it with this post.

Canadians on average pay very high investment fees and many are unaware of it: According to Investor Economics In 2023 Canadians paid an estimated $41 billion dollars in investment fees and expenses (across mutual funds and exchange traded funds (ETFs)), that’s about $1,000 per Canadian (many of whom don’t invest). Canadians held $1.9 trillion dollars in mutual funds and another ~400 billion in ETFs. The average all-in cost for an investor with $500,000 in a mutual fund was $10,227 per year or a shade over 2%. According to a FAIR Canada survey 77% of Canadian investors are concerned they are paying too high fees and 63% of Canadian Investors don’t understand the fees they pay. At least part of the issue is that investment fees and expenses are difficult to understand, and seldomly reported in a single aggregated figure to investors.

The good news is that management expense ratios (the biggest component of the costs) have declined significantly over the past 10 years, and further regulations go in effect in 2026 that will make the costs of investing and financial advice even more salient to investors, because only then can they assess whether or not it’s worth it.

There are 2 main categories of costs Canadians pay: (The Figures in brackets are relative sizes of cost buckets based on 2023 investor economics mutual fund data).

1) The costs of the financial product or investment implementation, these fees are paid to the institution and/or fund manager and can include:

• Management Expense Ratio (MER) of funds & ETFs which covers compensation and administration costs for the investment fund manager (~45% of average mutual fund cost)

• Other expenses including trading spreads, sales taxes, other operating expenses, and trading commissions and spreads ( ~15% of average mutual fund cost)

• The costs of embedded features such as insurance in segregated funds (Not relevant for mutual funds)

Product costs can vary from well less than 0.1% for a passively managed exchange traded fund (ETF), to 3%+ for actively managed segregated funds that include insurance-like features.

As famously put by Index investing pioneer John Bogle: “The grim irony of investing, then, is that we investors as a group not only don't get what we pay for, we get precisely what we don't pay for.”

2) The costs of advice or payments made to the financial/investment advisor who is serving the client

• This can include direct compensation in fee-based accounts. (Charged directly by advisors and not included in the costs of mutual funds)

• It often also includes indirect compensation where the costs of the advice are embedded in the product costs above such as trailing commissions in funds like A-series mutual funds (embedded in the management expense ratio). (~40% of average mutual fund cost).

The cost of advice can also vary from 0% (no advice), to upwards of 1.5%. Comparing the cost of advice is difficult as service levels vary significantly.

Ok so now we understand these 2 big buckets of costs lets better understand what are Canadians actually paying? For this analysis I used Morningstar’s 2025 Fund Fee Study and made some educated extrapolations.

I define the “Extra” cost as the cost over and above a low cost, self-directed exchange traded fund which can be purchased for ~0.15% or less.

1.1) Investment Style: (~0.6-0.8% extra for active management)

1.2) Proprietary higher cost products (~0.3-0.6%+ extra for captive products)

1.3) Embedded Insurance-like features (~0.8-1.5%+ extra for features like principal guarantees)

2.1) The cost of advice (0.7-1.3% extra for advice)

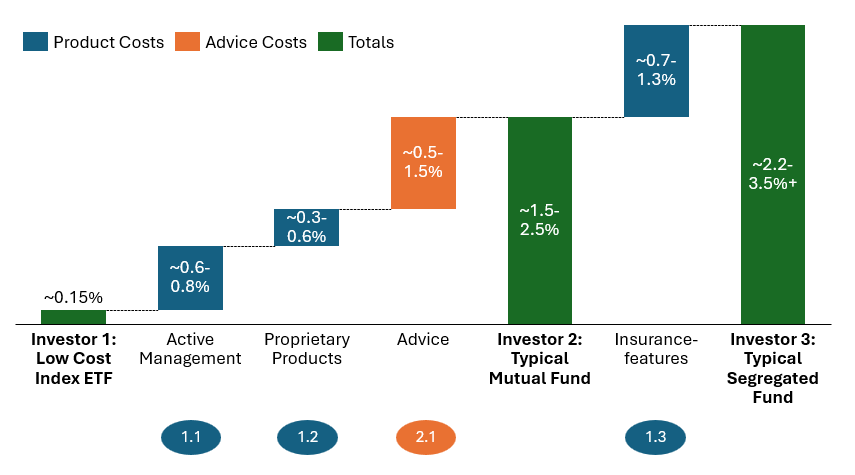

These costs can stack: The illustration below shows how 3 different investors with a similar portfolio of 60% global stocks & 40% bonds might pay very different fees.

Investor 1: Is a Do it yourself investor and has a low cost globally diversified ETF and receives no advice. They pay 0.15% per year, or $750 on a 500K portfolio

Investor 2: Holds very similar underling stocks and bonds through active mutual funds, and receives some advice, they pay ~2% per year or roughly 10K

Investor 3: Holds very similar underling stocks and bonds through segregated funds, they may receive advice and typically have some protections if their investments decline over the 10 years or more, they pay ~3% per year or roughly 15K.

Ok so all these costs can get expensive, let’s understand more what investors are paying for in each category.

1.1) Investment Style

Active investment strategies attempt to beat their benchmark performance by achieving higher risk-adjusted returns than could have been done by investing in the market. These organizations have highly compensated employees who are responsible for picking stocks and bonds that they think will perform better than average. There is robust academic literature that suggests that while many active managers can beat the market before costs, they rarely do so after costs and it’s impossible to know which managers will do so on a consistent basis.

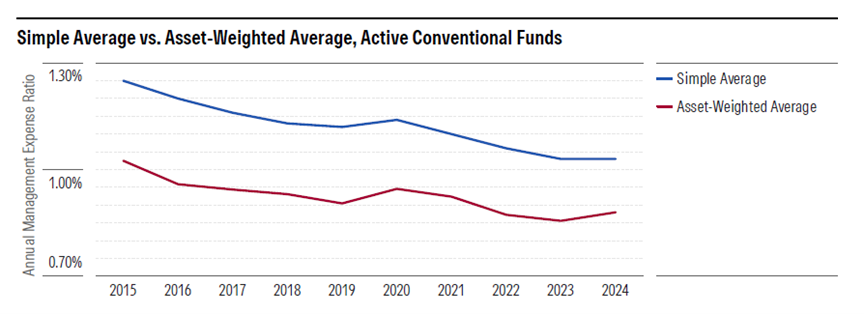

On an Asset Weighted basis, the typical cost to Canadians of an actively managed investment fund is ~0.9% (excluding the cost of advice). See Chart 1 Below.

Chart 1: Active management costs for all Canadian funds (excluding share classes where the cost of advice is embedded)

Source: Morningstar 2025 Fee study

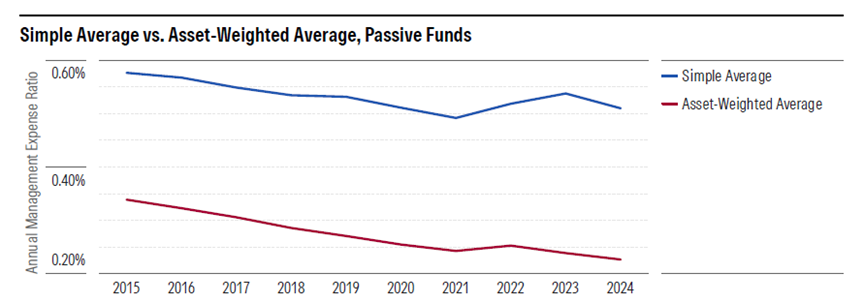

Passive investing (or index-based investing) is the alternative, in this style the investment manager buys all of the securities in an index or market, and earning similar returns to the benchmark. This style results in significantly lower costs (no expensive research and stock pickers). On an Asset Weighted basis, the typical cost to Canadians of a passively managed investment fund is ~0.2% (excluding the cost of advice). See Chart 2 Below.

Chart 2: Passive investment management costs for all Canadian funds (excluding share classes where the cost of advice is embedded)

Source: Morningstar 2025 Fee study

Active investing costs most Canadian investors at least .7% in additional fund management expense ratio per year with limited value. These funds also tend to have higher other expenses such as trading spreads and taxes, despite this and over 80% of Canadian Investments remain in actively managed funds.

Passive investments are gaining traction in Canada, but so too are private investments or “alternatives” such as private credit and private equity which also involve active management and typically significantly higher fees (especially for retail investors).

1.2) Proprietary, higher cost products sold to customers within an often captive distribution channel

This is the really challenging part of the asset management landscape in Canada (and I think the root cause of why so many Canadians are skeptical of financial institutions). An integral part of the profit model of large banks, insurance companies, and many asset managers is incentivizing or requiring their staff to recommend investment products that are also manufactured by that same organization, often at a higher cost to the investor.

This is often but not always combined with active management, however if investors do manage to buy a passive index portfolio from many of the large asset managers they will likely still pay significantly higher fees by using the institution’s product rather than a comparable independent passively managed product.

Please note we are not endorsing specific securities but consider this example: (this pattern persists across Canadian asset managers). VCN.TO is a Canadian Equity Index ETF with a MER of 0.06%, whereas the Scotiabank Canadian Equity Index Fund (BNS581.CF) has very comparable equity exposure but has a MER of 0.55%. That’s 0.5% of additional product/admin costs.

1.3) Embedded “insurance-like” features such as principal guarantees and death benefits

This deserves a post on its own, but as a general rule products sold by insurance companies that combine investment and insurance features come at a significantly higher cost than purchasing insurance and investments separately. For example Segregated Funds sold by insurance companies include insurance-like features such as guaranteeing 75% or 100% of the principle over a period of often 10 years or in the event of death of the policy holder. These funds often have MERs in excess of 3% and additional sales charges and commissions to cover the cost of advice. Segregated funds often also include the costs of active management, and proprietary products but the insurance features add an additional ~0.7-1.2% in further costs.

2.1) The cost of advice

Interestingly the cost of advice in Canada is reasonably concentrated around 1% of assets under management despite the level of service varying significantly, see chart 3 below.

Chart 3: Passive investment management costs for all Canadian funds (excluding share classes where the cost of advice is embedded)

Source: Morningstar 2025 Fee study

There is significant variability in the service levels that comes from this advice, ranging from an annual check-in to comprehensive financial planning. Paying for advice you aren’t receiving is clearly a bad deal for investors, however high-quality personalized advice can for many investors exceed the value of the cost of that advice (we’ll break this down in a future post). There’s also the complicating factor that if an investor finds an advisor they trust that is delivering valuable advice to them, they may be stuck with certain product costs because of the channel that advisor works with.

Ok great what does this all mean, well first the average Canadian investor really is paying ~2% fees for some combination of product costs and advice. As an newer investor or with a small balance that might be totally fine, but on a $500K portfolio $10K/year is a substantial claim on future retirement income and you deserve to understand what’s going into that fee (and what you are getting in return).

The good news is that costs are coming down both within categories and by a shift from active to passive funds. Furthermore, new legislation beginning in 2026 (Total Cost Reporting), will make the investment product costs and the costs of advice significantly more salient for investors and cover a broader range of products. Most investors will get their first glimpse of that data in early 2027 when they receive their annual investment statements followed by some tough conversations with advisors.

If you made it to the end thanks and happy holidays! This post was much deeper than planned, if you enjoyed this type of content please subscribe for more. As always happy to answer any questions at info@gybefinancial.ca.

If you found this article helpful please subscribe and/or share it with your friends and family who could benefit (I send a maximum of one article per month).

Planning for Your Death Is the Ultimate Act of Love: Simple steps to help you get started

Planning for the worst — incapacity, or death— is an act of love that relieves administrative and financial burdens for those who matter most to you. By preparing and having difficult conversations now, you can avoid unnecessary stress and potential conflict down the road.

My goal with this post is to distill a simple action plan for working professionals who might otherwise say “estate planning is only for the rich, I don’t need to worry about that right now”.

Thinking about your own death is uncomfortable — which is exactly why most people put it off.

Planning for the worst — incapacity, or death — is an act of love that relieves administrative and financial burdens for those who matter most to you. By preparing and having difficult conversations now, you can avoid unnecessary stress and potential conflict down the road.

*As always, this information is for education purposes only and is not intended as tax, legal, accounting, or investment advice. Your unique situation will vary!

My goal with this post is to distill a simple action plan for working professionals who might otherwise say, “Estate planning is only for the rich — I don’t need to worry about that right now.”

Before You Start: Key Concepts on Death & Taxes in Canada

For many financial assets, you can designate a beneficiary — these will pass directly to that person when you die.

The rest of your assets and liabilities form what’s called an estate.

There are no direct inheritance taxes in Canada, but your estate is responsible for your final tax bill which for many Canadians will be the largest they ever pay.

RRSPs and RRIFs are deemed to be withdrawn immediately before death (and taxed as income to the RRSP holder).

Non-registered investments and properties are deemed to be sold (resulting in capital gains tax on net gains).

Tax-free rollovers are generally available to spouses or common-law partners (and sometimes financially dependent children or grandchildren).

Probate is legal the process of validating a deceased person’s will. Probate fees of roughly 1.5% apply in Ontario to assets that flow through your estate (provincial rules and probate rates vary). Trying to avoid probate often creates larger tax and administration problems later.

Estate administration can take years — professional legal and financial support is highly encouraged.

Advanced planning can help reduce the emotional and tax burden at this difficult time, and can explore options may include living gifts, phasedRRSP drawdowns or taxable investment sales, and/or charitable donations.

Phew — that’s a lot to digest. But estate planning doesn’t have to happen all at once. Here are three practical Action Items to help you get started.

Action Item #1: Build a Family Money File — Create Order for the Unexpected

It’s common for a household to have 15 or more financial accounts across banking, investments, insurance, pensions, and credit cards. That can be tricky to navigate even when you’re the one who opened them — now imagine a loved one trying to sort it out without you.

The solution: Take a few hours to build a Family Money File. List all accounts and policies, including:

The institution, account number, and approximate balance

The names and contact information of key professionals (e.g., accountant, insurance agent, planner)

Save this file somewhere secure and ensure your partner and executor can access it. For households where one person handles most finances, this single act can dramatically reduce stress for the “non-money person.” It also serves as a great starting point for recurring family money meetings. If you are comfortable giving your loved one a way to access your phone, computer, and digital password manager in an emergency can significantly reduce the burden of closing online accounts.

Here’s a template I have used myself:Credit to Evan Neufeld, CFP

Action Item #2: Put in Place the Key Legal Documents — The “Big 3”

Every adult should have three key legal documents in place:

A Valid Will: Governs how your assets are distributed when you pass. It also appoints a personal representative (executor) to administer your estate, directs guardianship for children, and can establish testamentary trusts to distribute assets in stages (e.g., 50% at age 25, balance at 30). Dying without a valid will (intestate) delays an already long process and means your estate will be divided under provincial rules — not necessarily your wishes. If you need more motivation to get a will, read this

A Power of Attorney for Property: Authorizes someone you trust to manage your financial affairs on your behalf.

A Power of Attorney for Personal Care: Authorizes someone you trust to make medical and lifestyle decisions on your behalf. Consider also expressing your care wishes (for your PoA to act on) in a written healthcare directive.

Pro Tips:

You can use the process of establishing your will as a chance to discuss your parents’ plans — and to talk with your executor and beneficiaries about your own.

Choosing your executor is a big decision best thought through with an experienced professional. This role involves a significant time and emotional burden. Ensure your executor is willing and capable now and in the future, and ideally lives in the same province. Choosing multiple executors (for example all of your children) can feel like an act of trust and love, but will make it more complex to settle your estate (many in-person coordination and signature meetings).

Review these documents every 3–5 years or after major life events (marriage, divorce, births, deaths, new business, inheritances).

Online tools like Willful or LegalWills.ca are better than nothing however my family chose to work with a lawyer and found real value in the process — they asked thoughtful questions we hadn’t considered and helped us navigate tricky “what if” scenarios.

Decide whether your Power of Attorney takes effect immediately (requires deep trust) or is “springing” upon a doctor’s determination of incapacity (which can lead to delays/ care challenges).

Action Item #3: Review Your Beneficiary Designations — Keep Paperwork and Intentions Aligned

Many financial products — RRSPs, TFSAs, life insurance, pensions — allow you to designate a beneficiary. These assets typically bypass your estate and go directly to the named person.

You can update designations by submitting new paperwork with the financial institution that holds your accounts.

Things to keep in mind:

Coordinate designations with your will — conflicting instructions can cause administrative headaches and disputes.

For registered accounts, you can name your spouse as a successor annuitant, allowing both the account and contribution room to transfer tax-deferred.

Be mindful of potential tax implications when transferring RRSPs or appreciated non-registered assets (your estate is responsible for the tax bill).

Minor children can’t directly inherit funds, ensure your will names a guardian

If in doubt, you can name your estate (or not name a beneficiary) and direct distributions through your will.

Closing Thoughts

Don’t worry if you can’t check off everything right away — just get started.

Planning for the unexpected is about care, clarity, and compassion. These steps may feel heavy, but they lighten the load for those you love most.

If this topic has you thinking about your own plans (or your parents’), drop me a note at chaz@gybefinancial.ca — I’d be happy to help you chart a calmer course forward.

If you found this article helpful please subscribe and/or share it with your friends and family who could benefit (I send a maximum of one article per month).

💼 Thinking of Going Solo? Practical thoughts for navigating your finances through the transition to independent contracting/consulting practice.

Independent contracting or consulting is a big life choice, it also has many financial planning considerations. Can I afford to do this? Should I Incorporate? How should I manage year one cash flows. We offer practical tips to navigating this exciting transition.

Working independently in service-based businesses is growing in both popularity and accessibility. We will focus on some of the financial considerations, but this is much more than a financial decision. This process can feel daunting, but it’s totally possible—and it can have some amazing benefits.

*As always, this information is for education purposes only and is not intended as tax, legal, accounting, or investment advice. Your unique situation will vary!

Big Question #1: Can I afford to go independent now?

What is your personal “burn rate”? How long could you live comfortably if you had zero revenue? Money stress can stifle creativity and push you toward non-ideal clients and contracts.

Is your family on the same page? Early entrepreneurship can mean sacrifices—financially and personally. It’s critical to go in with an aligned front.

What is your end game? How you set up your practice and finances is intricately related to your goals. A lifestyle practice has very different investment needs than a multi-person boutique.

Pro Tips:

Test the market: For your services long before you take the leap. Starting with a signed contract gives you clarity, validation, and early momentum.

Build a runway: If you can generate solid leads, aim for 6–9 months of personal financial runway. You can shorten this by firming up engagement(s) prior to taking the plunge

Recommended Resources:

📘 The Irresistible Consultant’s Guide to Winning Clients by David A. Fields — a practical and entertaining guide to building a client pipeline based on relationships and “Right-Side-Up” thinking. I should have a referral fee from this author by now :).

🌐 Staffing platforms like Catalant, Toptal, Umbrex, or Upwork can help you find first projects as can working your network of past clients and boutique consulting firms working in a similar space.

Big Question #2: Should I incorporate — and if so, when?

Are your revenues and retained profits sufficient to justify the costs and complexity? Incorporation can unlock significant tax deferral (12.2% small business corporate rate in Ontario vs. 53.5% top marginal tax rate) but costs $2,500+ per year and adds administrative work. The financial benefits to incorporation are greatest if you’ll have excess savings in your corporation after paying yourself enough to covering personal expenses and contributions to your tax-sheltered investment accounts (TFSA & RRSP).

What is the risk profile of your business and how will you manage it? Incorporation creates a separate legal entity and can protect your personal assets. Errors & Omissions insurance can further increase protection.

Do your clients play a role in the decision? Some clients require incorporated contractors. It’s also easier to sell an incorporated business. On the flip side, if your revenue is concentrated with a single client, be cautious of CRA’s personal services business rules, as non-compliance can be very costly.

Pro Tips:

Avoid premature incorporation: Sole proprietorships are simpler, less costly, and allow you to deduct most business losses personally. You can incorporate later once your business has matured.

If you do incorporate, seek advice: Consider professional advice for things like share structure, whether to include a spouse, accounting setup, payroll, and fiscal year-end timing.

Recommended Resources:

🎥 Financial planner Jason Pereira explains this trade-off well: YouTube: Should You Incorporate?

🏢 RBC’s Ownr can be a cost-effective alternative for simple incorporation and annual filings—but professional advice is still valuable (and can be used in parallel).

Big Question #3: How to best manage your cashflow and compensation in year 1?

How will you pay yourself in Year 1? As a business owner, you decide how and when to pay yourself. For your first year, dividends can reduce admin, offer a one-time personal tax deferral, and may avoid “double-paying” the employer CPP portion if you already had T4 income earlier that year.

When to register for HST/GST? You must register once you exceed $30K in revenue over four consecutive quarters, once you register you begin collecting sales tax on behalf of the CRA, you also start the clock on deducting input tax credits (ITCs). When you purchase inputs and supplies or hire subcontractors who charge HST you get input tax credits for the HST you paid, you ultimately will remit the net amount of sales tax collected less input tax credits to the CRA. If your taxable inputs are low it makes sense to explore the “Quick Method” of HST accounting (more below).

Are you forecasting your tax bill? Early income without source deductions feels great—but plan ahead. Example: earning $150K net in Year 1, paying yourself $100K in dividends, and skipping installments could lead to ~$45K in taxes and HST due within the first 3–4 months of the following year.

Pro Tips:

Consider dividends in Year 1 if your CPP was maxed by a prior employer: You could otherwise make up to $4.4K in duplicate employer CPP contributions that don’t add anything to your CPP benefit.

Consider the Quick Method of HST accounting: If HST paid on input costs is less than 1/3 of the HST you collect, ask your accountant about the Quick Method of HST accounting as it could save you time and allow you to keep a portion of the HST you collect.

Plan ahead for taxes: Ask your accountant or financial planner to project your total Year-1 tax bill (personal, corporate, and HST) and set aside the funds in advance.

Recommended Resources:

📘 CRA Guide RC4058 — Quick Method of Accounting for GST/HST — short, clear, and surprisingly useful.

💻 CRA’s Payroll Deductions Online Calculator: Visit here can help you estimate your payroll deductions if you choose to manage this.

Over the longer term, how you pay yourself—and whether you invest inside your corporation—can have a massive impact on your financial future (Salary has many underrated benefits). These decisions should be grounded in a comprehensive long-term financial plan and re-visited annually. I’ll dig deeper into this topics in upcoming posts.

Closing thoughts:

Gosh that was a lot for a single post, and it truly feels like we are just scratching the surface on each of these important topics. If you are thinking about the financial planning considerations of independent consulting drop me a line at chaz@gybefinancial.ca so we can discuss your unique circumstances.

If you found this article helpful please subscribe and/or share it with your friends and family who could benefit (I send a maximum of one article per month).

Chaz’s Personal Gybe: Launching a Financial Planning Business

You are doing what??? oh… interesting… good luck!

If my goals were to maximize my income or professional clout I’ve taken a pretty significant turn off the well worn path …

In my first blog post I break down my logic in starting Gybe Financial.

You are doing what??? oh… interesting… good luck!

After a period of deep contemplation I recently shared with my personal & professional network my decision to launch Gybe and their reaction was curious, supportive, and perhaps a little surprised.

If my goals were to maximize my income or professional clout I’ve taken a pretty significant turn off the well worn path of working at a prestigious consulting firm, getting a MBA, and then rising through the corporate ranks.

I strongly believe there’s more to life than money and status, at the same time money can be an incredible tool in helping you get the most out of your one precious life.

Gybe will be my conduit for helping others get their finances working for them in a way that lets them live their most authentic lives (whatever their goals may be).

For those who are curious to learn why a strategy consultant to leading pension plans & investors is jumping into personal financial planning, I’ll break down my logic in a 5 section bullet-pointed framework like a good consultant would do :).

My intention with this blog will be to focus on delivering valuable insights to my clients and broader audience but this first blog post is admittedly self-indulgent (and hopefully a reminder I can look at in tough times).

1) I’ve always had a deep interest in personal finance and expect my passion and knowledge to compound:

I am a personal finance nerd through and through. I voluntarily subjected myself to the QAFP exam (~300 hours of coursework before deciding to make a career of this) and was captivated with tax planning module.

I’m also fascinated by how people in similar situations can have completely different goals and financial outcomes.

I’ve been able to find that wonderful bliss of “flow” in the financial planning work I’ve done to date and I hope that never fades.

My family has been consistent savers and disciplined evidence-based investors for many years, part of what has made starting Gybe possible

2) There is a tremendous opportunity to deliver impactful, conflict-free, advice in Canada:

I will make a dramatic oversimplification of the Canadian Asset Management landscape below to illustrate a point, no offence intended! Across all models there are great firms and great advisors! (More blog posts to come here).

The “Old Way”: Hire a bank financial advisor (or large investment firm) whose service is primarily focused on investment management. This approach can come with a trusted long-term relationship, personalized advice, and behavioral support to navigate the market’s inevitable ups and downs. The challenge is relatively high cost that can often be embedded in high product fees. (80% of Canadian’s privately held investment funds were held in mutual funds (~1.8 Trillion Dollars in assets as of 2020) with an asset weighted management expense ratio (MER) of 1.7% per year). FP Canada’s return assumptions for a balanced portfolio before fees are approximately 5.3% so 1.7% means nearly 1/3 of projected returns are lost to fees (not great when compounding over a lifetime!). The other issue is that the quality and depth of non-investment advice that is anchored in a financial plan is variable in this channel, for example <15% of advisors in Canada registered to sell investment products hold the CFP or QAFP designations.

The “New way”: Transfer your investments to a discount brokerage or Robo-Advisor and build yourself a low cost portfolio (Haven’t we all seen the Questrade adds), this can certainty lower costs but shifts the onus on the investor to remain steadyhanded through market cycles, and leaves them turning to the internet for managing the other elements of their finances like saving, managing taxes, planning for retirement etc. Study after study has shown that individual investors make sub-optimal decisions and typically fail to achieve market level returns. So while you may get lower fees, it takes a special level of knowledge and temperament to get great outcomes.

Gybe and other financial planning focused firms seek to offer a “Better way” (for many Canadians): The client pays directly on a fixed fee/ or hourly basis to get personalized advice in the context of a financial plan with no product sales. The client can implement a low cost, globally diversified investment portfolio that is suited to your goals with the confidence that their plan is aligned with their goals and behavioral support along the way.

Finally I’m grateful for the Financial Planning Association of Canada and specifically the advice only planner community who have blazed a trail under this new model, demonstrating that Canadians value and are willing to pay for this advice. This way of practicing is still rare but not completely unknown: Of the ~20,000 FP Canada Approved Financial Planners less than 2% are practicing in an advice-only model. I have found many mentors eager to share tips and business practices.

3) Financial planning aligns with my “talent spikes”:

A career in consulting is great for getting lots of pointed feedback on what your professional strengths are, I have been described as:

Being highly analytical, retaining lots of information, and slotting that into the big picture of what we are trying to accomplish

Being patient, trustworthy, and generally optimistic with the people I interact with

Having a knack for teaching and coaching and breaking complex concepts down in a practical and understandable way

Having a bias towards action, and getting stuff done in the context of resource constraints & competing priorities

4) My professional experience and network will bring a unique and well-rounded perspective:

I have advised some of Canada’s largest and most sophisticated investment funds, the odds are stacked against us retail investors so we need to keep things simple!

I have spent the last ~3 years working closely with some of Canada’s largest Defined Benefit pension administrators and built an in depth understanding of how pensions (and their administrators) work

I have the technical acumen for robust financial planning: Top score on QAFP exam, MBA in Finance, and I worked as a teaching assistant for accounting courses during my undergraduate degree

I worked as a corporate executive at a fortune 500 company for several years, I know what it’s like to have may competing priorities and need simple and clear advice

I have started and managed my own incorporated business, optimizing cash flows and corporate investing

5) Both the Journey and Destination are exciting:

Personal financial planning is not likely to be as financially rewarding as consulting, However I expect to draw deep fulfillment from helping my clients meet their goals

I am excited by the prospect of building a business where I can serve clients in a way that is values aligned and maintains my personal balance beyond work

I plan to build Gybe into an enduring organization that outlasts myself and positively impacts many Canadians but am open to the inevitable twists and turns along the way

Finally I’m incredibly grateful for the rewarding career I’ve had to date and the support from my wonderful wife, family and friends to take this leap at a time where most folks my age (especially parents of with children under 5 like myself) are overwhelmed by their personal and financial responsibilities.

If this post resonated with you please subscribe to receive posts directly to your inbox , and don’t hesitate to book some time to talk all things personal finance