A space to learn more about personal financial planning. You can expect regular posts covering a range of topics from tips & tricks, to big decisions that matter for DB Pension Members, Incorporated Business Owners, DIY Investors, and those making big life pivots.

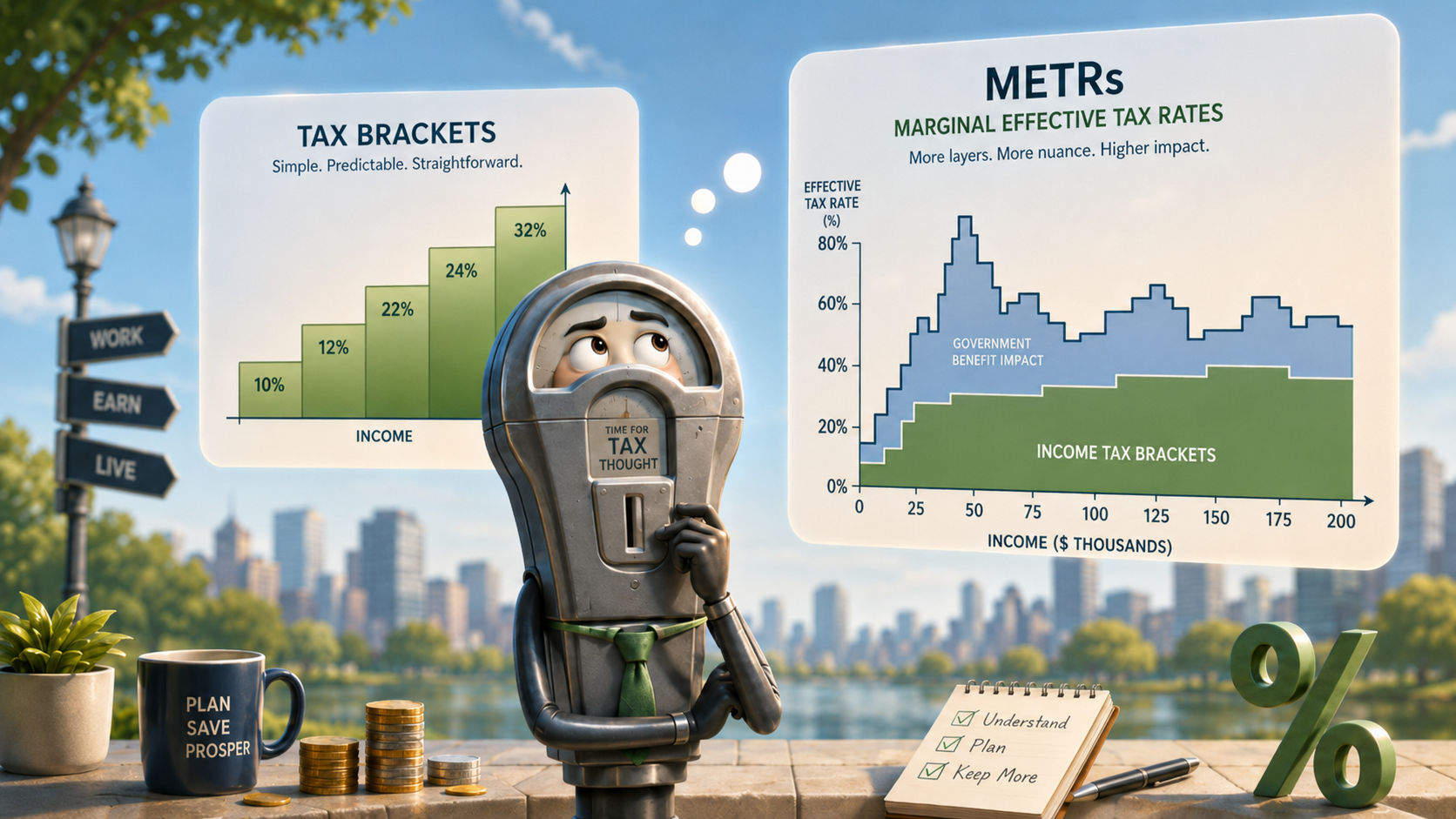

What’s your M.E.T.R.? … and other ways “managing income to a tax bracket” can go wrong.

Planning taxable income around a certain tax bracket often misses nuances in how income is calculated, tax deductions, and finally income tested government benefits. It’s an effective and valuable process but not as simple as just eyeballing a tax bracket and hoping you end up close to that.

This post summarizes some of the pitfalls I have seen for clients trying this approach on their own.

“I try to keep my taxable income under the “X”K combined tax bracket” sounds smart and can make great sense if done correctly, and for the right set of circumstances

Managing your taxable income to a bracket sounds simple but almost everyone I’ve worked so far who is attempting to manage taxable income (even with the help of accountants) is missing some part of the required nuance. It’s tricky stuff, and requires a deep and reasonably comprehensive multi-year understanding of your finances and life.

But first one big caveat, this article is not personalized tax advice, many details and nuances are omitted for simplicity. It’s a framework for how to think about annual taxable income planning from someone who came from outside the personal finance world and has had to learn it (I’m still learning every day).

First in order to manage your income you need some control over it. The degree of control you have over your taxable income varies a lot depending on your personal situation including:

How much cash flow do you need to live on (If you need to spend everything you earn and don’t have other resources taxable income planning will be difficult)?

Are you adding to, repositioning, or withdrawing from your investments?

Does your income naturally vary from year to year and can you earn more/less on demand?

What type(s) of income do you have (investments, employment, business etc.)?

What tax deductions (if any) are available to you

Generally the more of the above are true the more opportunity you will have for taxable income planning. But most Canadians have some opportunity to manage their income through RRSP contributions and eventual withdrawals.

Why might you manage your taxable income if you could?

Canada has a progressive taxable income system, in general lower taxable income that is smoothed across years and more evenly split amongst partners delivers a more efficient result than very high or lumpy income. Consider 2 example families that both earn 400K in total household income over 2 years (all employment income in Ontario and ignoring gov’t benefits for simplicity). Family 1 has one partner earn 400K in year 1 and both partners earn zero in year 2 , family 2 has 2 partners working for 2 years each for 100K/year. Family 2 will pay nearly ~70K less in personal income taxes, leaving more money to live and invest.

I find most clients intuitively understand this part, it’s what gives rise to the desire to do some taxable income planning e.g. avoiding the nearly 54% marginal tax rate on taxable income above ~258K, or the ~5.5% income tax rate jump on income above ~117K. For those who do have significant ability to manage their taxable income there are strong benefits to doing so. The problem is that there are a couple of wrinkles that many DIY tax planning efforts miss notably: Tax treatments of different types of incomes, tax deductions, and income-tested government benefits.

This is a nuanced topic (And I will necessarily leave out a bunch of details) but I’ll do my best to highlight the most common misinterpretations when estimating your tax bracket for income planning purposes. There’s a whole separate set of considerations for what deductions you may be entitled to, and how you might try and legally split income with a partner or stage it over multiple years (also important but not for today!).

Wrinkle 1: Estimating taxable income.

The first complication is that not all types of income are treated the same when calculating taxable income. Employment income and interest income are generally included dollar-for-dollar.

Eligible dividends from taxable Canadian corporations — for example, dividends from public companies such as TD Bank or Enbridge — are treated differently. These dividends are “grossed up” by 38%, meaning that $1.00 of eligible dividends counts as $1.38 of taxable income. This does not mean eligible dividends are necessarily taxed more heavily overall. The gross-up is paired with a dividend tax credit, which is intended to recognize that corporate tax has already been paid. However, that credit reduces tax payable after taxable income has already been calculated. This distinction matters when taxable income itself affects other calculations, thresholds, credits, or benefits.

Realized capital gains (think from the sale of taxable investments or a second property) have 50% of the gain included in taxable income.

So for a hypothetical couple who work together in a family business and where each family member has a 70K salary, 20K of eligible dividends received, 10K ineligible dividends, and a 50K capital gain on the sale of their portion of a jointly owned rental property there’s some nuance to their income estimation. For those following the math it would be 70K + 1.38*20K + 1.15×10K + 50%*50K = 134.1K of income for tax purposes before considering deductions.

There’s then a second step of calculating deductions which serve to reduce taxable income. Two frequent deductions are RRSP contributions, and eligible childcare expenses but there are many more. Deductions reduce your taxable income dollar for dollar (subject to the cap on the deduction). Let’s imagine one of our family members was planning to deduct 10K in RRSP contributions and is eligible to deduct 10K in daycare expenses (only available to the lower earner). Now their taxable income is $114K. They might compare that to the combined tax brackets in Ontario and say, great I’m just under the ~117K cutoff for the next tax bracket (and from jumping to an over 43% marginal tax). And my RRSP deduction is primarily coming from the above 117K tax bracket thus reducing my current tax bill by 43% for every dollar contributed. But even if they managed to do all of the above correct they might still be missing some nuance: Enter income tested government Benefits

Before we go there though between the 2 steps above, someone who is “ballpark estimating” their taxable income can go significantly awry so doing a mid-year check with an accountant or financial planner before making any big moves like triggering capital gains or paying yourself a bonus can definitely help!

Now for Wrinkle 2: Income tested government benefits

The Federal and Provincial Governments offers many generous benefits for taxpayers. Many of these benefits are “Income-tested” meaning that they stop or are gradually “clawed-back” as your personal net taxable income or adjusted family net income (AFNI) exceed certain thresholds. The tricky part is that the cutoffs for these benefits don’t always match up with the tax brackets you may have been planning for, and the way they are calculated varies by benefit as does the benefit year.

A DIY tax planner might compare their 114K personal taxable income that to the combined federal/Ontario tax brackets and say, “Great, I’m just under the roughly $117K threshold where the marginal rate on ordinary income jumps from about 38% to about 43%.” That may be a useful observation, but it still may not tell the whole story. The tax bracket is only one layer. The next layer is whether the same income affects income-tested government benefits, credits, or clawbacks.

The most famous example is the infamous OAS Recovery Tax. For July 2026-June 2027 payments the government will “Claw back” 15% of your OAS payments for every dollar of 2025 personal worldwide net income that exceeds the cutoff of $93,454. So for your next dollar earned above this threshold in addition to personal income tax of ~43% you’d be losing 15% of your OAS benefit. This means your marginal effective tax rate (M.E.T.R) inclusive of government benefits could be ~58% which is even higher than the top combined federal/provincial personal tax bracket. My personal view is that it is good policy not to pay OAS to seniors who don’t need it, but the current system sure does create some strange incentives and tax complications.

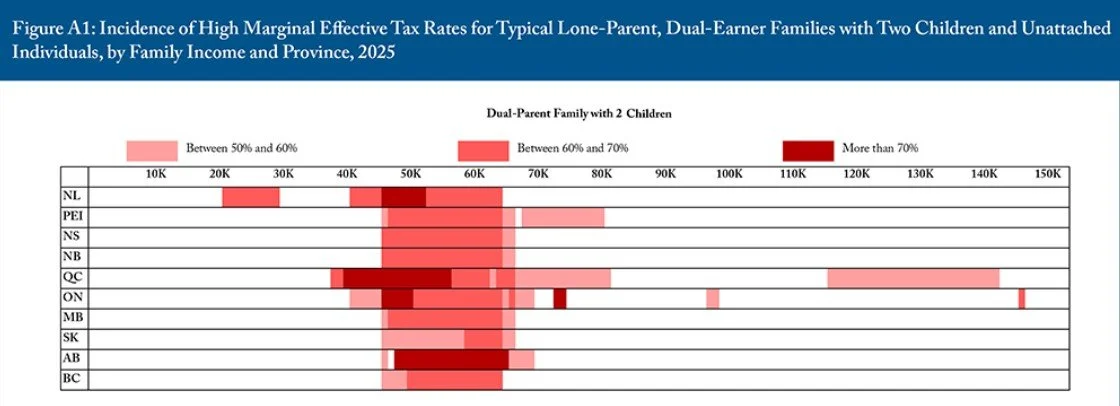

Now our dual earning couple above was a long way from retirement, but they do have 3 children under age 6 and are eligible for the Canada Child Benefit which is an income tested benefit based on Adjusted Family Net Income. I’ll save the details for another post but even at ~228K of AFNI they are still entitled to ~$4K/year in tax free Canada Child Benefit Payments. And more interesting is that their Marginal effective tax rate is 8% higher than a simple “tax bracket analysis” would suggest.

Canadians who are most likely to see the the biggest differences in their marginal effective tax-rates and their simple tax brackets are parents with modest incomes, and single income seniors who are close to the OAS Clawback Thresholds.

I find this visual extremely helpful from the CD Howe Report “The Clawback Trap” which shows how M.E.T.R.s can exceed 50% for 2 child modest income households (Whom traditional financial advice would say never contribute to your RRSP when you are in a low tax bracket). Link to the report here: https://cdhowe.org/publication/the-clawback-trap-how-canadas-benefit-system-can-undermine-work-and-saving/

There are many other benefits, especially if you will have a modest family or personal income (see above the 40K-80K) AFNI range is pretty severely taxed on a M.E.T.R. basis across Canada for parents.

Finally, life changes, and financial and tax-planning should be a long-term focused process that anticipates a certain amount of uncertainty. It doesn’t do much good to perfectly fit into a desired tax bracket for 3 years only to blow past it by orders of magnitude to cover a major expense in the 4th year. This is where wholistic multi-year planning can make a big difference.

All this is to say that DIY tax planning is helpful, but it’s rarely as simple as “I just pay myself $xK to stay below the $yK tax bracket”.

If you found this article helpful please subscribe and/or share it with your friends and family and broader network, it really helps me continue to write these.

Finally if you think annual taxable income planning might be appropriate for your situation, but I’ve successfully talked you out of doing it without some help, I am currently including annual taxable income consultations for all of my ongoing advice-only financial planning clients you can book a complimentary introductory video call here.

💼 Thinking of Going Solo? Practical thoughts for navigating your finances through the transition to independent contracting/consulting practice.

Independent contracting or consulting is a big life choice, it also has many financial planning considerations. Can I afford to do this? Should I Incorporate? How should I manage year one cash flows. We offer practical tips to navigating this exciting transition.

Working independently in service-based businesses is growing in both popularity and accessibility. We will focus on some of the financial considerations, but this is much more than a financial decision. This process can feel daunting, but it’s totally possible—and it can have some amazing benefits.

*As always, this information is for education purposes only and is not intended as tax, legal, accounting, or investment advice. Your unique situation will vary!

Big Question #1: Can I afford to go independent now?

What is your personal “burn rate”? How long could you live comfortably if you had zero revenue? Money stress can stifle creativity and push you toward non-ideal clients and contracts.

Is your family on the same page? Early entrepreneurship can mean sacrifices—financially and personally. It’s critical to go in with an aligned front.

What is your end game? How you set up your practice and finances is intricately related to your goals. A lifestyle practice has very different investment needs than a multi-person boutique.

Pro Tips:

Test the market: For your services long before you take the leap. Starting with a signed contract gives you clarity, validation, and early momentum.

Build a runway: If you can generate solid leads, aim for 6–9 months of personal financial runway. You can shorten this by firming up engagement(s) prior to taking the plunge

Recommended Resources:

📘 The Irresistible Consultant’s Guide to Winning Clients by David A. Fields — a practical and entertaining guide to building a client pipeline based on relationships and “Right-Side-Up” thinking. I should have a referral fee from this author by now :).

🌐 Staffing platforms like Catalant, Toptal, Umbrex, or Upwork can help you find first projects as can working your network of past clients and boutique consulting firms working in a similar space.

Big Question #2: Should I incorporate — and if so, when?

Are your revenues and retained profits sufficient to justify the costs and complexity? Incorporation can unlock significant tax deferral (12.2% small business corporate rate in Ontario vs. 53.5% top marginal tax rate) but costs $2,500+ per year and adds administrative work. The financial benefits to incorporation are greatest if you’ll have excess savings in your corporation after paying yourself enough to covering personal expenses and contributions to your tax-sheltered investment accounts (TFSA & RRSP).

What is the risk profile of your business and how will you manage it? Incorporation creates a separate legal entity and can protect your personal assets. Errors & Omissions insurance can further increase protection.

Do your clients play a role in the decision? Some clients require incorporated contractors. It’s also easier to sell an incorporated business. On the flip side, if your revenue is concentrated with a single client, be cautious of CRA’s personal services business rules, as non-compliance can be very costly.

Pro Tips:

Avoid premature incorporation: Sole proprietorships are simpler, less costly, and allow you to deduct most business losses personally. You can incorporate later once your business has matured.

If you do incorporate, seek advice: Consider professional advice for things like share structure, whether to include a spouse, accounting setup, payroll, and fiscal year-end timing.

Recommended Resources:

🎥 Financial planner Jason Pereira explains this trade-off well: YouTube: Should You Incorporate?

🏢 RBC’s Ownr can be a cost-effective alternative for simple incorporation and annual filings—but professional advice is still valuable (and can be used in parallel).

Big Question #3: How to best manage your cashflow and compensation in year 1?

How will you pay yourself in Year 1? As a business owner, you decide how and when to pay yourself. For your first year, dividends can reduce admin, offer a one-time personal tax deferral, and may avoid “double-paying” the employer CPP portion if you already had T4 income earlier that year.

When to register for HST/GST? You must register once you exceed $30K in revenue over four consecutive quarters, once you register you begin collecting sales tax on behalf of the CRA, you also start the clock on deducting input tax credits (ITCs). When you purchase inputs and supplies or hire subcontractors who charge HST you get input tax credits for the HST you paid, you ultimately will remit the net amount of sales tax collected less input tax credits to the CRA. If your taxable inputs are low it makes sense to explore the “Quick Method” of HST accounting (more below).

Are you forecasting your tax bill? Early income without source deductions feels great—but plan ahead. Example: earning $150K net in Year 1, paying yourself $100K in dividends, and skipping installments could lead to ~$45K in taxes and HST due within the first 3–4 months of the following year.

Pro Tips:

Consider dividends in Year 1 if your CPP was maxed by a prior employer: You could otherwise make up to $4.4K in duplicate employer CPP contributions that don’t add anything to your CPP benefit.

Consider the Quick Method of HST accounting: If HST paid on input costs is less than 1/3 of the HST you collect, ask your accountant about the Quick Method of HST accounting as it could save you time and allow you to keep a portion of the HST you collect.

Plan ahead for taxes: Ask your accountant or financial planner to project your total Year-1 tax bill (personal, corporate, and HST) and set aside the funds in advance.