Could Ongoing Advice Only Planning help improve your retirement outcomes? A case study on the cost of advice.

I want to be careful to clearly delineate the cost and potential value of financial planning and advice (and not simply paying for investment management).

A good planner can help you tease out your financial goals, build wealth efficiently, save on taxes , and put major life decisions in the context of your financial life. The peace of mind and accountability partnership can be the difference in achieving your financial goals and for many people is well worth paying for. There’s a mix of hard $ savings and returns and soft benefits and it’s impossible to quantify in advance, but my experience so far has been a very high return on investment relative to initial planning fees.

Ok so if paying for high quality ongoing personalized financial advice can make sense for some people, what does it actually cost and how do those costs impact your financial outcomes?

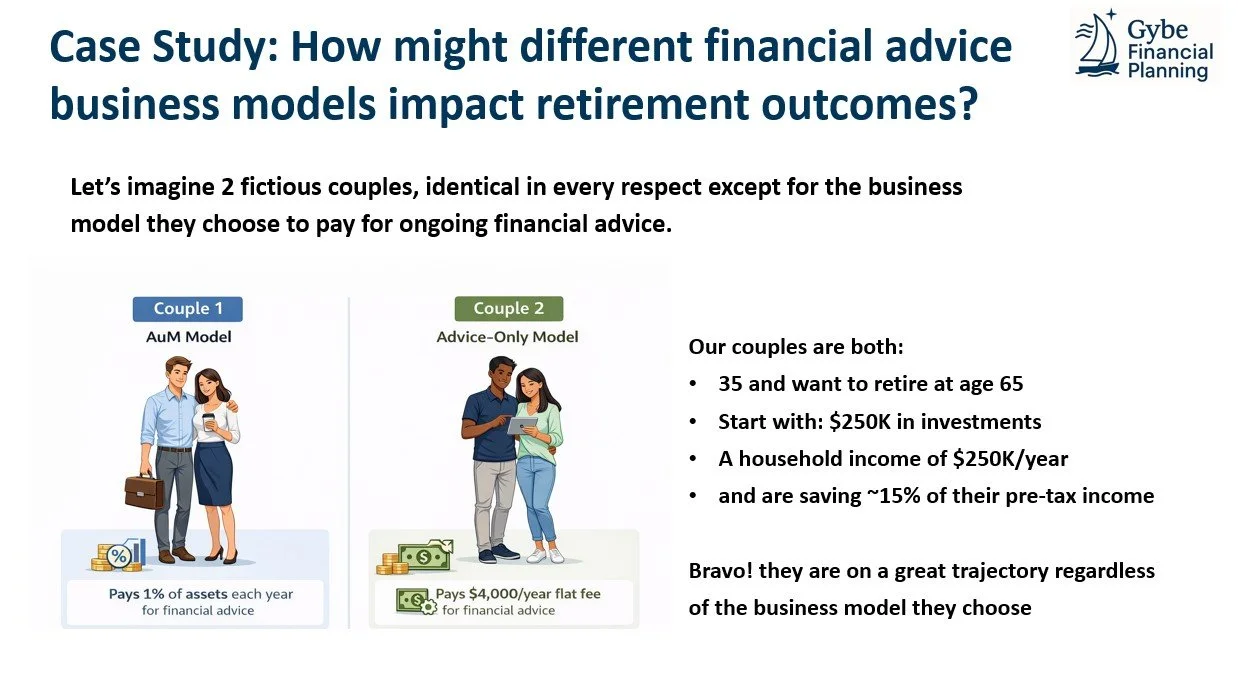

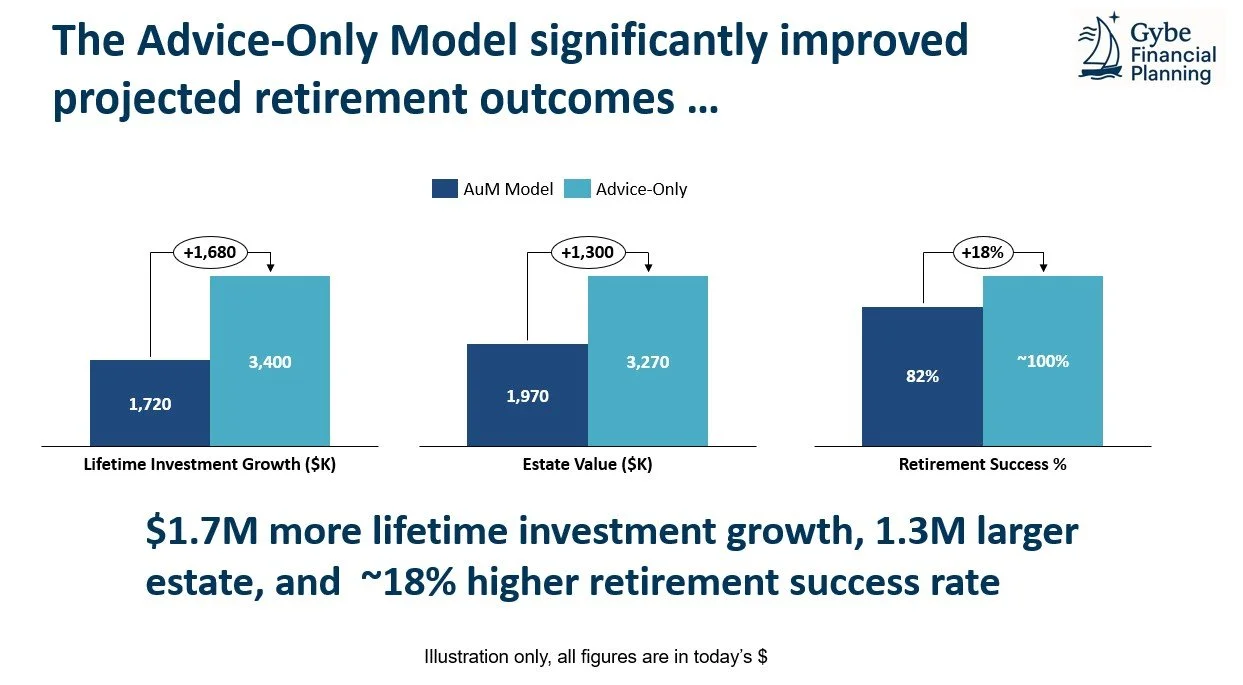

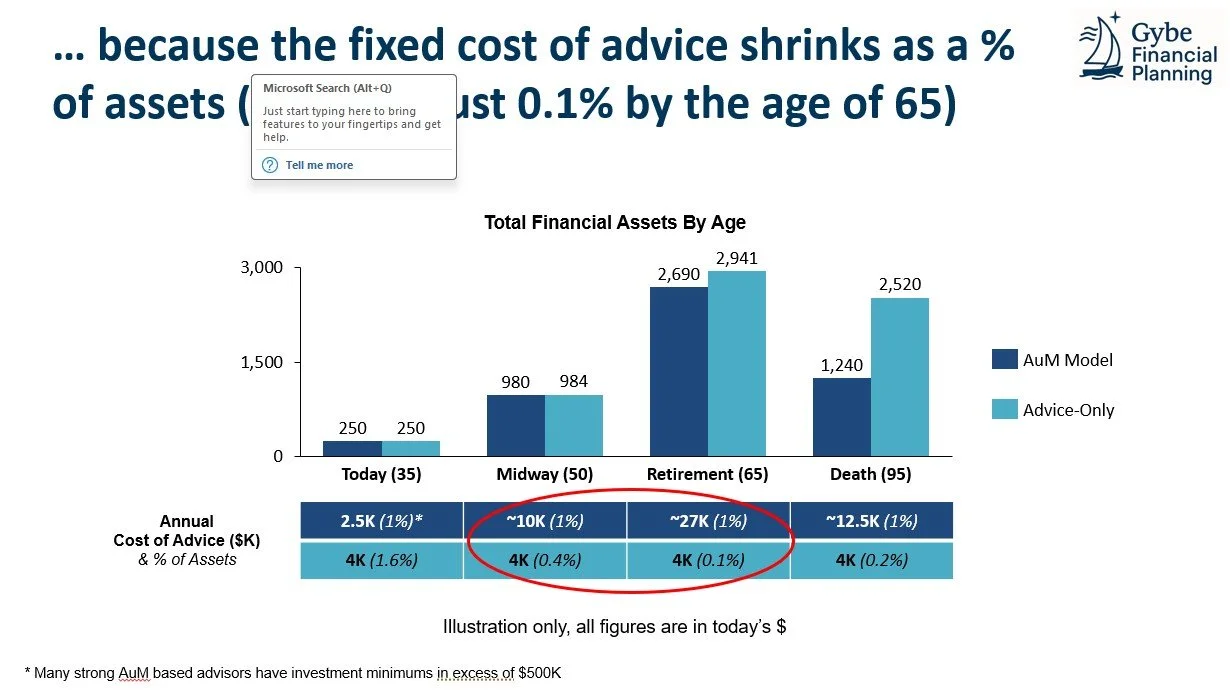

It made sense intuitively that once you have a higher value of assets paying a fixed fee versus a % of assets would likely be more cost effective, but It wasn’t immediately obvious to me that paying a fixed fee over your lifetime would potentially lead to better retirement outcomes. So I decided to test it with a good old fashioned case study.

An Important simplifying assumption I am making is that their before fee-performance is identical as are the financial moves they make in their life (based in part on the quality of the advice) are equal. I think this is totally possible for disciplined self-directed investors but many are not able to avoid tinkering.

These are definitely not identical services, nor are they the only ways Canadians can arrange their personal finances, but it’s helpful to know on cost-only basis how these different service models compare.

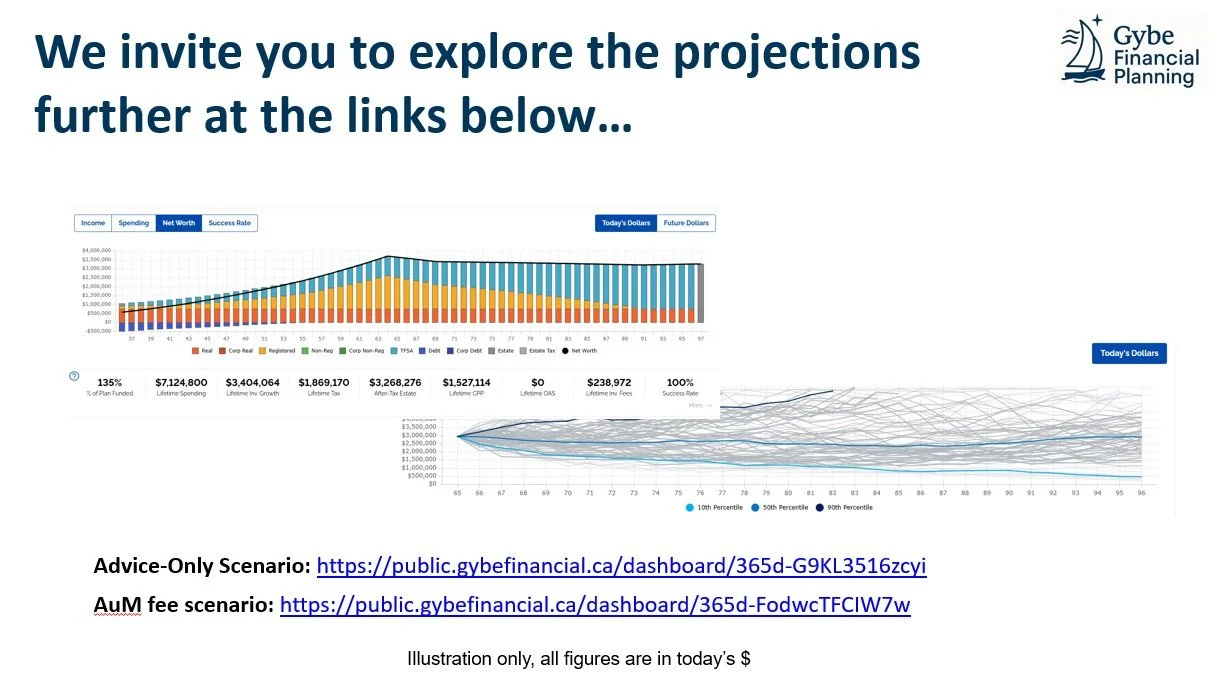

For those interested in the more detailed assumptions and/or exploring the modelling software you can download the case study slides here

As a bonus below I’ve outlined several “options” that exist for Canadians in accessing advice and their typical costs

Option 1-Investment Manager that focuses on high cost (proprietary products) or active investing (picking stocks)my personal view is that even high quality comprehensive planning would struggle to overcome ~2%+ ongoing fees from a financial outcome standpoint: Please refer to my previous blog post… and don’t do this!

Option 2-Investment Manager that focuses on low-cost evidence based investing and comprehensive financial planning. Typical cost is ~1% of assets under management for advice and another ~0.2% for investment implementation. This way you are mostly paying for advice, which can be very valuable. This is a great option for many, especially if you aren’t comfortable managing your own investments and/or would be tempted to sell in market downturns. One such example is PWL Capital whose Chief Investment Officer Ben Felix, is one of the premiere personal finance educators. There are significant synergies in combining financial planning and investment management including dynamic withdrawal strategies.

Option 3- Ongoing Advice-Only Financial Planning (AoP). This is often a “fixed fee” model of ~2,500-5,000+ per year which on significant investment balances can be much less than 1% per year. The level of planning (and hence value add) is also usually directly related to the fees charged. In this model the client manages their own investments or pays separately for investment management. Most AoP planners are not securities licensed and cannot discuss or recommend specific investments but can add value on asset allocation and assessing the costs of your current investments.

Option 4- Do it Yourself Investments and/or Robo-Advisors (No/Limited Advice): I’ll be the first to admit, not everyone needs to pay for advice. Self-directed investing can be had for 0.1%-0.5% of your assets. For many people especially those in their early accumulation phase, who are already on a strong track of saving in their registered accounts, and have the temperament to stick to a low-cost buy and hold investment strategy this can be a great option. It’s where things start to get complicated (either through registered accounts maxing out, contemplating big changes in income, self employment or incorporation, managing an inheritance, or thinking about retirement dates and retirement income planning) where thoughtful advice can really shine.

If an ongoing advice-only financial planning model could make sense for you, you’ve come to the right place

At Gybe most clients we have partnered with so far have had short-term financial opportunities that are significantly larger than the initial financial planning fee. Relatively simple strategies have brought our clients years closer to achieving their financial goals, which has been great validation for the business model. It’s also why to date Gybe has been offering clients a 100% unconditional money-back guarantee on our financial planning services (and we haven’t had any issues yet). If you’d like to explore what a 90-day financial planning engagement might look like for your situation please book a complimentary introductory session here

If you found this article helpful please subscribe and/or share it with your friends and family.